European green technology funding for shipowners is a gift for Chinese shipbuilders. European shipbuilding associations call f’or changes to the provision green subsidies, which are benefiting China.

‘The EU doesn’t understand there is shipbuilding in Europe,’ said Sea Europe director of trade and competitiveness Vincent Guerre

EUROPEAN shipbuilding associations are demanding that the European Union and governments pay more attention to localised shipbuilding before it disappears entirely. While, at the same time, they want “green” funding provisioned to shipowners ordering “green” newbuildings to support the business case for European shipyards, and not benefit Chinese shipyards.

“With European elections in June, which will see new commissioners appointed to the European Commission, we have been busy building our case. We want the new Commissioner for Industry to ensure we

regain shipbuilding capability and view the sector as critical for economic security,” Vincent Guerre, director of trade and competitiveness at shipyards and marine equipment association Sea Europe, told Lloyd’s List.

Guerre says that a long-term lack of understanding at both national government level, and at the EU, about shipbuilding has been a boon for China.

“The EU doesn’t understand there is shipbuilding in Europe. It has failed to remedy the trade distortions stemming from the massive support granted by China to its shipbuilding industry, notably through dumping and subsidies. As a result, Chinese shipyards are 30-40% cheaper than European shipyards.”

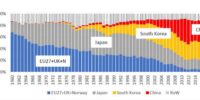

The decades-long decline of shipbuilding production in Europe is a complicated subject involving many factors. A glance at shipbuilding output data provided by Sea Europe confirms how globally uncompetitive the sector has become.

Global shipbuilding output percentage by region

So given the seemingly insignificant shipbuilding production of European shipbuilders, why should politicians care?

Western politicians have woken up to the risks of a more belligerent China and Chinese manufacturing dominance. Therefore, Guerre is more confident the EU will listen to concerns about the lack of support for European shipbuilding.

“The issues of shipbuilding were not on the European political agenda for years but many things have changed over the past five years. For example, economic security was never seen in EU papers before, but it is now. Nevertheless, the EU is slow moving and likes to do a lot of papers.”

With no demands on where a shipowner orders its newbuildings to benefit from green subsidies, which include the European Green Deal, the situation remains a gift to China.

In addition to EU funding, national governments are also paying out to European shipowners for the construction of “green” vessels with alternative fuel propulsion systems.

A newbuilding project for dual-fuel chemical tankers for operation in European coastal waters, won a green subsidy of $1.7m per ship for their German owner from the Federal Ministry for Digital and Transport Affairs.

With average newbuilding pricing 40% cheaper in China compared with Europe, unsurprisingly the entire order was won by a Chinese shipyard.

“European shipyards don’t even try to compete now for most cargo vessel newbuilding contracts, which is why we are out of the market for bulk carriers, containerships and tankers. Europe may still be strong in cruise for example, but we need to consolidate what we have.

“We want the EU to help us consolidate a business case for vessel segments where China is not yet dominant, but we have to acknowledge we won’t get the big volumes and instead concentrate on high value ships.”

Earlier this month, European shipbuilding received a boost when the two world’s largest cruiseship operators, Carnival Corporation and Royal Caribbean Group, each placing orders for mega cruiseships at Germany’s Meyer Werft and France’s Chantiers de l’Atlantique. They were the first ships to have been ordered by the US-listed companies since 2019.

When considering the eye-watering contract price of the vessels, upwards of $1bn apiece, the importance of European shipbuilding makes more sense than if looking at mere tonnage output data.

Reinhard Lüken, managing director at Verband für Schiffbau und Meerestechnik (the German Shipbuilding and Ocean Industries Association) says that when cruiseship orders hit their peak between 2016 and 2018, European shipyards won orders valued at a combined $20bn. This order in value was at the same level as China and South Korea.

“While our market share of global shipbuilding went up this was distracting as we were stilllosing shipbuilding capacity.”

Lüken cites the loss of valuable orders for passenger ferries and ro-ro cargo vessels to China as an example of where European shipbuilders have gone from world dominance to almost insignificance.

“Ferries had been chiefly a European business and one of our biggest markets but now that’s almost gone. What is the reason? Shipbuilding nations in eastern Europe such as Romania could easily compete with China on labour cost, but at the end of the day it comes down to government policies.

“The Chinese government has a very clear strategy about shipbuilding, but we didn’t understand what was behind it. At first we believed it was about employment and development, but we now think there is a substantial security component to it.”

In the past decade China has built the world’s largest naval force as it sought greater influence on the world stage.

“The expansion of China’s navy was an aspect we hadn’t seen coming but there is also an argument that low Chinese shipbuilding prices for merchant vessels have kept global transport costs lower — China’s low-cost export manufacturing model only works when transport costs are low.”

Lüken argues that the lack of support from the EU and governments, and little effective scrutiny of unfair competition by Asian shipbuilders has not been very smart.

“Europe’s coastline is twice as long as China and the US put together. We have so much maritime trade but it seems we have given up on shipbuilding almost voluntarily. This needs to be revisited. Technical sovereignty is very important.”

Lüken noted the example of British shipbuilding. Until the 1960s, the UK was the world’s leading shipbuilding nation but was largely nationalised in the late 1970s, with ultimately disastrous consequences.

“It takes some determination to go from global market leader to practically zero within S0 years. In the UK it had a lot to do with too much focus on service industries — financiers in London are just not interested in manufacturing.”

Despite accusations of unfair Chinese competition and complaints to the World Trade Organisation, there is little evidence that China’s shipyards are receiving any direct state subsidies.

“It’s difficult to trace subsidies to Chinese shipyards. While we haven’t been able to prove it there are many ways the sector can be subsidised via the supply chain.”

US think tanks evaluated Chinese state subsidies to shipbuilding and estimate that around $200bn has been provided to the sector over a 15-year period.

Meanwhile, incentives for European shipowners to order in China include not just low pricing but financial incentives from Chinese state banks, which provide tax-based leasing on very competitive terms.

The world’s second-largest shipbuilding nation, South Korea, has made no secret of its fight back against what it perceives to be unfair competition from China.

In November, South Korea’s Ministry of Trade, Industry and Energy launched its “K-Shipbuilding Strategy for Next-Generation Market Dominance”, which will provide $547m over five years. It appears to be a clear move by the South Korean government to protect its shipbuilders’ technological edge over China.

“The South Korean government has been putting a lot of money into its industry, but this is transparent since South Korea is a democracy.”

Billions of dollars are understood to have been poured in to South Korean shipbuilding over the past 15 years as most shipyards have been unable to turn a profit.

“Even if there were no subsidies provided to Chinese or South Korean shipbuilders would Europe be competitive? No, because we don’t have their economy of scale. The damage has been done.”

Lüken said that rather than trying to recapture market sure, European shipbuilders should continue to focus on certain high value, complex, vessel types and on domestic demand.

“I believe we can be successful with optimised production. With big enough numbers of vessels of the same design we can close the gap. We won’t be building super-large cargo ships but we can remain competitive for small and medium-sized cargo vessels and of course ferries — i.e. everything that supplies services for European services. Renewable energy also needs a huge number of offshore vessels to service it in the future.

“I think we can organise the shipbuilding industry much better than today. But to be successful, European policy makers need to understand we should not make the mistakes of the past.”